Walmart vs. Target: Which Retail Giant Is the Better Buy for 2025?

The retail sector is entering 2025 in very different circumstances than it was just a few years ago. Tariff tensions are increasing, and consumer spending patterns are changing.

In the face of these headwinds, retailers that can strike a balance between scale, value, and innovation will be best positioned to capitalize on the next phase of growth. Two household names that sit at the top of this competitive market are Walmart (WMT) and Target (TGT).

Both have different strategies for growth, digital transformation, and customer engagement. Let’s find out which retail stock offers the best opportunity now.

The Case for Walmart Stock

With a market cap of $766.6 billion, Walmart remains the largest retailer in the world by revenue. Its size remains its most significant advantage, bringing it closer to joining the exclusive $1 trillion market cap club. The retail giant operates around 10,500 stores and clubs in over 19 countries.

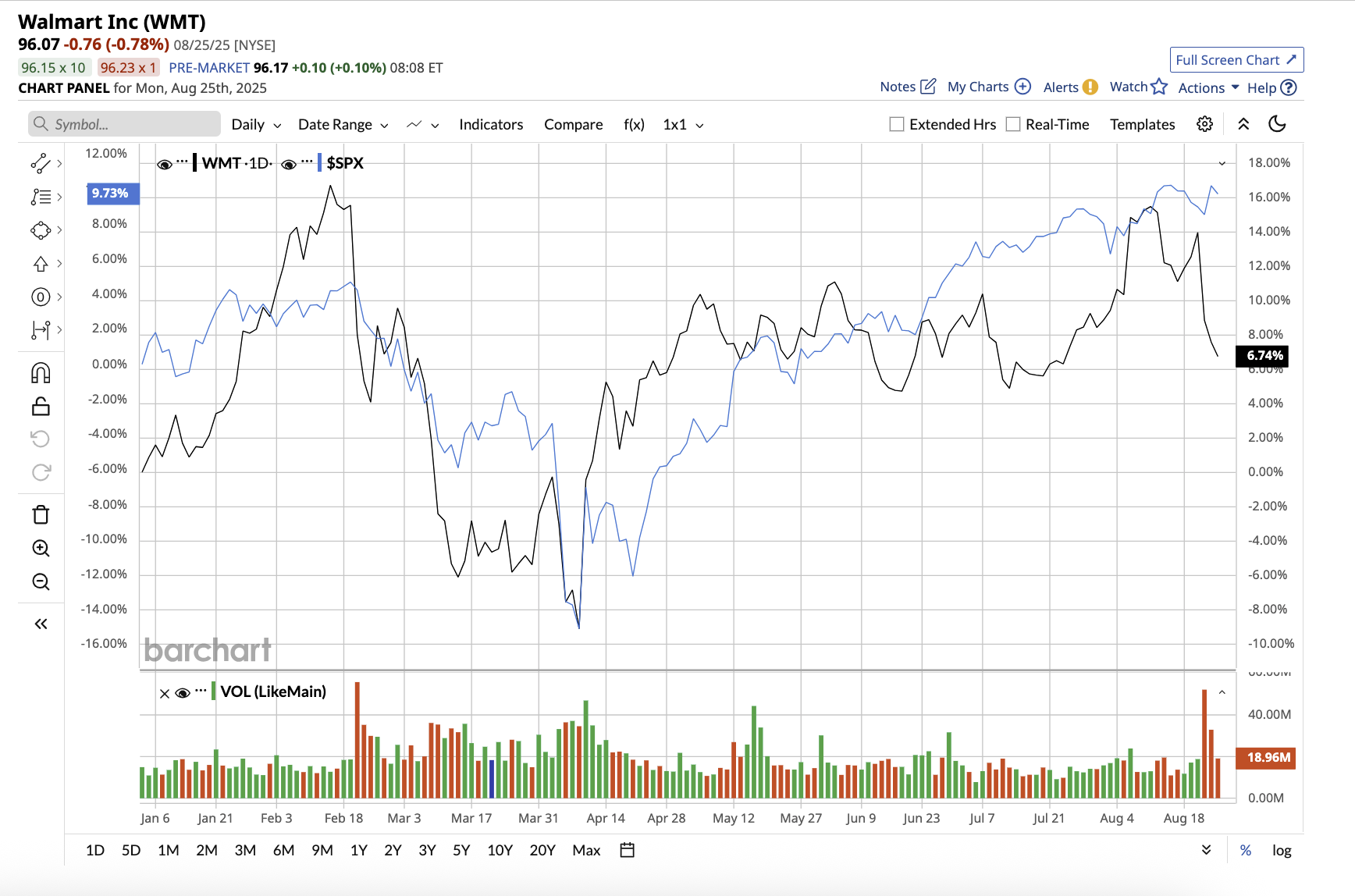

Walmart’s stock is up 5.8% year-to-date, compared to the S&P 500 Index’s ($SPX) gain of 9.6%.

In the second quarter, total revenue increased by 4.8% to $177.4 billion, while adjusted earnings per share increased by 1.5% to $0.68. The company’s e-commerce segment stood out once more, delivering 25% global growth, with Walmart and Sam’s Club outperforming expectations. Walmart increased comparable sales by 4.6% in the U.S., with strong performance in the apparel, media and gaming, and automotive categories. Sales increased by 10.5% in international markets, driven by strong performances in China, Walmex, and Flipkart.

Walmart is continuing to reshape its business model by expanding into higher-margin areas. Membership income increased by 15%, while global advertising increased by 46%, with contributions from VIZIO. Walmart’s continued investment in artificial intelligence (AI) was a key highlight of the quarter. Walmart is developing AI-powered “super agents” to transform its operations and customer experience.

Besides being a value stock, Walmart’s defensive nature also appeals to passive income investors during uncertain economic conditions. The company has earned the title of Dividend King by consistently increasing dividends over the last 53 years. Its dividend payout ratio of 32% suggests the dividends are sustainable for now.

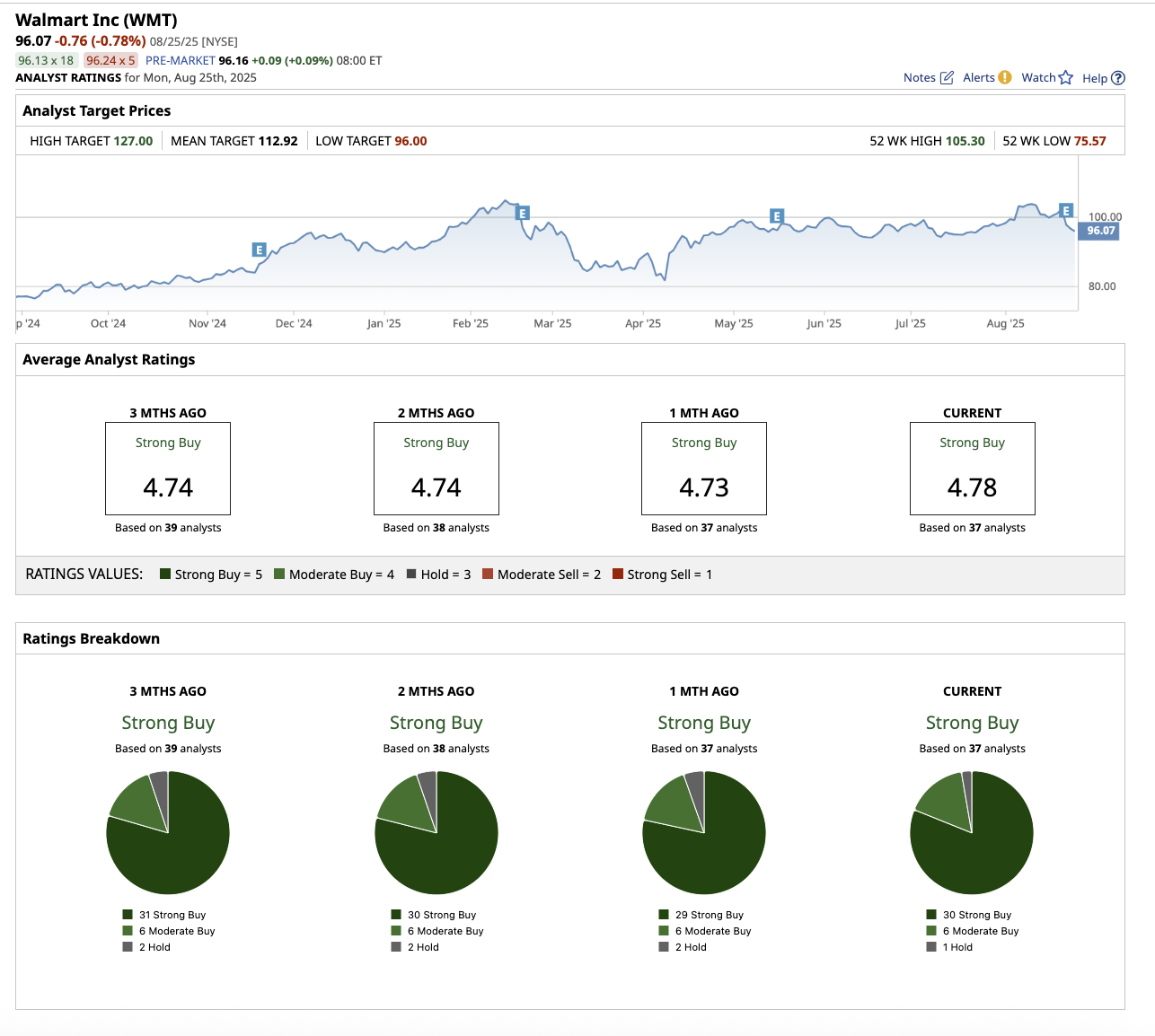

Overall, on Wall Street, Walmart stock has earned a “Strong Buy” rating. Out of the 37 analysts covering WMT stock, 30 have a “Strong Buy” recommendation, six rate it a “Moderate Buy,” and one recommends it is a “Hold.” Its average price target of $112.92 suggests upside potential of 17.5% from current levels. Its Street-high estimate of $127 implies potential upside of about 32.2% in the next 12 months.

The Case for Target Stock

Valued at $44.1 billion, Target is a large American retail chain that sells a wide range of products, including clothing, groceries, electronics, home goods, and household essentials, both in physical stores and online. It is known for its low prices, trendy merchandise, and easy one-stop shopping experience.

On Aug. 20, along with the second quarter results, Target announced that the company is entering a pivotal new chapter as long-time CEO Brian Cornell prepares to hand over the reins to Michael Fiddelke, the chief operating officer, effective Feb. 1, 2026. The leadership change occurs at a time when the retail giant is dealing with tariff volatility and consumer shifts. A sudden C-Suite leadership change, combined with an internal transition, spooked investors, causing Target’s stock to plummet. Target’s stock is down 29% so far this year.

During the earnings call, incoming CEO Michael Fiddelke acknowledged, “We’re not realizing our full potential right now.” He outlined three priorities for returning Target to profitable growth: establishing merchandising authority, improving the guest experience, and leveraging technology and speed. In the second quarter, net sales fell 0.9% year on year to $25.2 billion. Adjusted earnings per share (EPS) were $2.05, down from $2.57 the previous year, with management attributing the majority of the decrease to tariffs and inventory costs. Looking ahead, Target reaffirmed its full-year guidance for low single-digit comp declines and adjusted EPS of $7 to $9, compared to $8.86 in 2024. The consensus earnings estimate is $7.40 per share for the year.

Target also has a reputation as a Dividend King, having increased dividends for 54 consecutive years, with the most recent increase of 1.8% to $1.14 per common share. It has a dividend yield of 4.8%, which is higher than both Walmart’s yield of 0.98% and the consumer staples sector average of 1.89%. Its payout ratio of 57.1% is also reasonable, leaving room for expansion.

During the earnings call, the current CEO also reminded investors of Target’s structural advantages, which include nearly 2,000 well-located stores in all 50 states and a $31 billion owned brand portfolio. In addition, the company has partnerships with world-class companies such as Apple (AAPL) and Starbucks (SBUX), and it operates one of the largest loyalty programs in the country, Target Circle.

These assets, combined with a profitable and growing digital business, provide a solid foundation for Target’s next phase under new leadership.

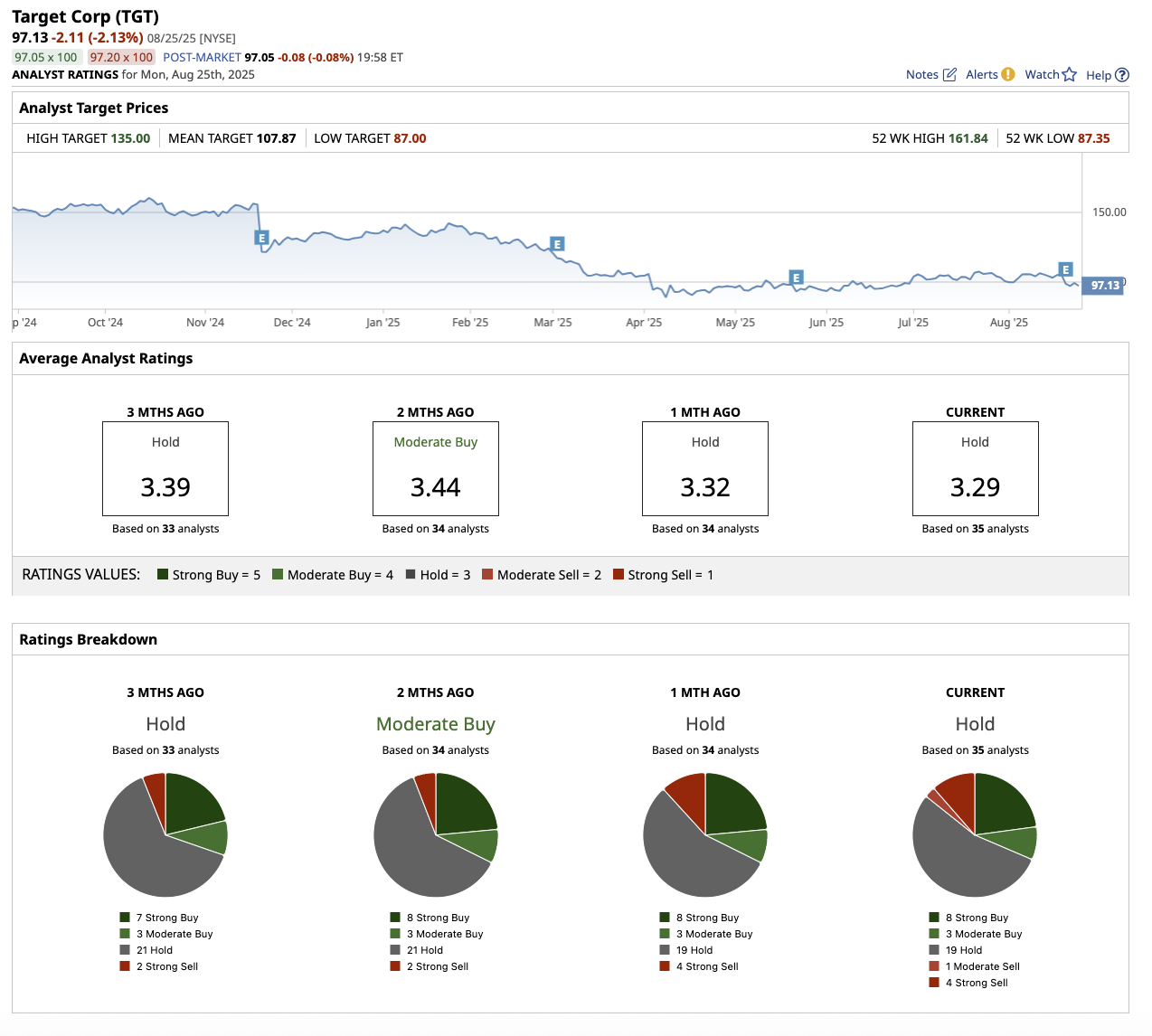

Overall, Wall Street holds a cautious stance on TGT stock, rating it a “Hold.” Of the 35 analysts covering the stock, eight analysts rate it a “Strong Buy,” with three rating it a “Moderate Buy,” 19 rating it a “Hold,” one suggesting a “Moderate Sell,” and four rating it a “Strong Sell.” The average target price of $108 implies upside potential of 11% from current levels. Plus, its high target price of $135 suggests the stock can rally as much as 39% over the next 12 months.

Which Retail Stock Is the Better Buy?

Walmart appears to be the safer, more reliable option. Its grocery dominance, investments in AI and automation, and expanding advertising business serve as strong growth drivers while remaining resilient during downturns. Furthermore, the company is a consistent dividend payer. For risk-averse investors looking for consistency, Walmart remains the clear choice.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.